[ad_1]

(Bloomberg) — Policymakers from Washington to Frankfurt head into the ultimate quarter of 2023 with tentative grounds for optimism that their struggle towards inflation is making progress.

With Federal Reserve chief Jerome Powell and his European Central Financial institution counterpart Christine Lagarde each resulting from communicate within the coming week, buyers will scrutinize any response from them to a transatlantic double whammy of information that provided hints of cheer.

Friday’s stories confirmed euro-zone core inflation — which strips out risky parts similar to vitality — working on the slowest tempo in a 12 months, and hours later, the Fed’s most popular measure of underlying value progress was revealed have risen the least since 2020.

With a authorities shutdown averted on Saturday, US central bankers are set to see one other spherical of that knowledge sequence, in addition to different inflation numbers, earlier than their determination on Nov. 1. The numbers launched to this point may enable them to begin constructing a case to chorus from a November charge hike.

The ECB will solely have a fuller model of the September inflation quantity to go on earlier than its Oct. 26 gathering, with each the report for October and the estimate of third-quarter progress scheduled for after the assembly.

An additional enhance in borrowing prices isn’t at the moment anticipated in October, and Friday’s report could begin to undermine any push for an ECB hike in December.

Powell will be part of Philadelphia Fed President Patrick Harker for a round-table dialogue with staff and small-business leaders on Monday. Regional Fed presidents Loretta Mester, Raphael Bostic and Mary Daly are additionally scheduled to talk within the coming week.

Lagarde, the ECB president, will ship the welcome tackle on Wednesday to a convention hosted by her establishment. Vice President Luis de Guindos will communicate the identical day in Cyprus, and different audio system for the week embrace chief economist Philip Lane and central-bank chiefs from Germany and France.

What Bloomberg Economics Says:

“The ECB has most likely completed elevating rates of interest. Quite a few measures of underlying value will increase are falling, surveys are pointing to a big deterioration in exercise and credit score extension is weaker than it was within the depth of the euro disaster. Nevertheless, the ECB will nonetheless want a very long time to have ample confidence to decrease charges.”

—David Powell, senior economist. For full evaluation, click on right here

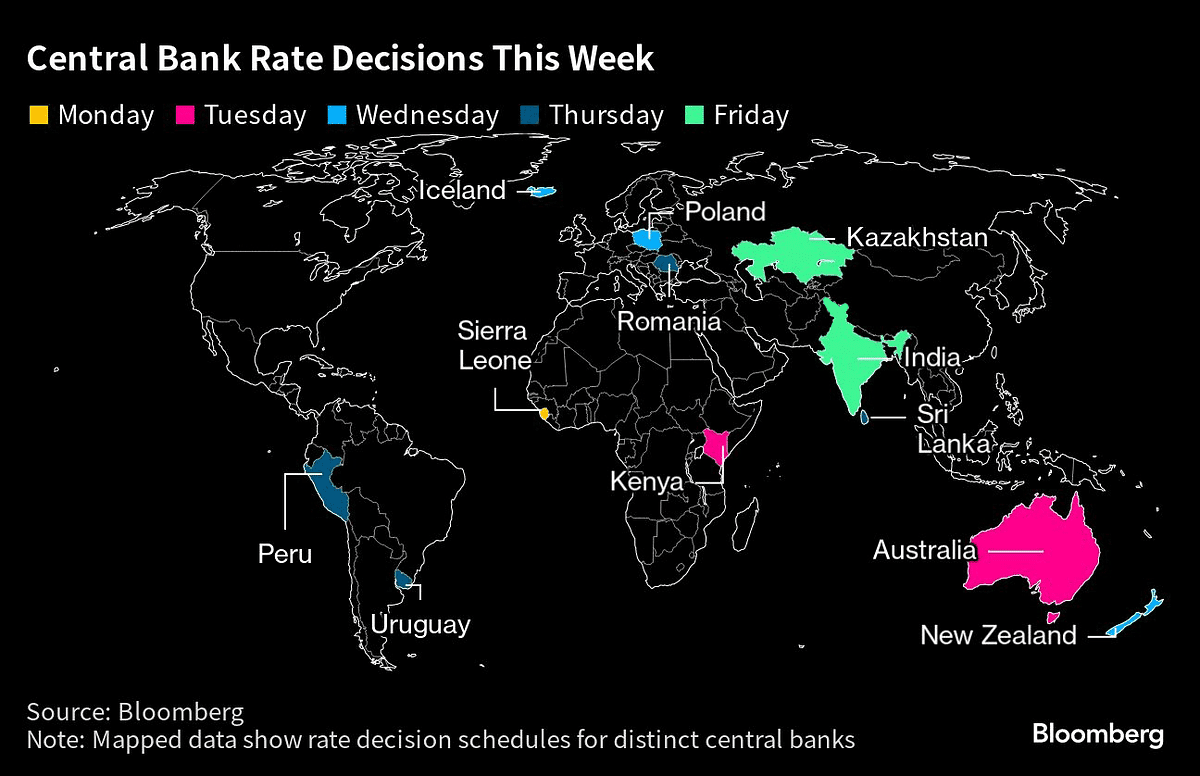

Elsewhere, a number of central-bank choices are due around the globe, with charges more likely to be unchanged from Australia to India.

Click on right here for what occurred final week and under is our wrap of what’s arising within the world economic system.

This week’s financial knowledge features a pair of high-profile stories on the state of employment. August’s JOLTS report on Tuesday and September’s nonfarm payrolls on Friday are anticipated to point out a markedly looser labor market.

The ratio of job openings to unemployed individuals — a key barometer of job-market tightness for the Fed – most likely declined to 1.4, in line with Bloomberg Economics. Hiring doubtless got here down sharply final month after the summer time’s non permanent bump within the leisure and hospitality sector from Taylor Swift and Beyonce live performance excursions.

Personal-sector numbers can even be in focus.

On Monday, the Institute for Provide Administration’s manufacturing index is anticipated to point out an eleventh straight month of contraction. ISM’s index of companies exercise, due Wednesday, is seen exhibiting barely slower progress.

Additionally on Wednesday, knowledge from the ADP Analysis Institute are projected to point out moderating progress in private-sector employment.

Trying north, Financial institution of Canada Deputy Governor Nicolas Vincent will communicate to Montreal’s Chamber of Commerce because the central financial institution weighs a current inflation uptick towards the backdrop of a slowing economic system.

Jobs knowledge for September will present an necessary guidepost for the financial institution after the August report blew previous expectations with double the anticipated employment good points and wage progress at 5.2% on the 12 months.

China is about for a week-long vacation, a break which may be a litmus check for consumption exhibiting how a lot individuals are keen to journey and spend. Forward of that, Saturday’s PMI knowledge confirmed manufacturing exercise returned to enlargement for the primary time in six months, one other signal that elements of the economic system are discovering their footing once more.

South Korean commerce numbers on Sunday confirmed a hunch in exports eased additional in September — a constructive signal that world commerce is regaining floor. PMI figures come on Monday, together with from Indonesia, Malaysia, Thailand and Vietnam.

On Tuesday, the Reserve Financial institution of Australia meets for the primary time underneath new Governor Michele Bullock, with central bankers anticipated to carry charges regular. The board could talk about the opportunity of some type of quantitative tightening.

That shall be adopted by New Zealand’s central financial institution charge determination Wednesday. Analysts forecast no change there or from the Reserve Financial institution of India on Friday. Thailand, the Philippines, South Korea and Taiwan will launch inflation figures throughout the week.

Tankan knowledge from the Financial institution of Japan on Monday will point out the newest state of company confidence, whereas Japanese wage knowledge on the finish of the week may have implications for financial coverage relying on how a lot pay progress continues to lag inflation, a key level of concern for the BOJ.

Europe, Center East, Africa

Within the UK, the Financial institution of England’s Choice Maker Panel survey shall be launched on Thursday, informing officers on value pressures within the economic system. Policymakers scheduled to talk within the coming week embrace Catherine Mann and Deputy Governor Ben Broadbent.

Industrial knowledge could draw consideration within the euro zone, with German exports and orders due towards the top of the week. French manufacturing numbers shall be printed on Thursday.

Swiss inflation could creep up towards the central financial institution’s 2% ceiling in a launch on Tuesday.

Within the Nordics, Sweden’s Riksbank on Monday will reveal the minutes of its current determination to lift charges and preserve the door open to a different transfer.

Throughout Europe and past, a number of charge choices are scheduled:

On the identical day, Turkish knowledge will doubtless present inflation accelerated to 61% in September, in line with a Bloomberg survey of analysts. That’s even because the central financial institution hikes charges considerably to struggle the nation’s cost-of-living disaster.

Chile’s August’s GDP-proxy studying posted on Monday could present the economic system stumbled in August after July’s better-than-expected studying. Exercise is extensively anticipated to rebound within the fourth quarter with out triggering central financial institution alarm bells.

In an analogous vein, the September shopper value report will doubtless present inflation slowed for a tenth month, greater than sufficient to maintain Banco Central de Chile on monitor for a 3rd straight charge minimize in October, from the present 9.5%.

Peru’s central financial institution is anticipated to increase its easing cycle with a second straight quarter-point minimize to 7.25%. Peru’s annual inflation slowed greater than anticipated in September, to five.04%, and central financial institution chief Julio Velarde expects it to ease to three.8% by year-end.

In Colombia, the minutes of Friday’s central financial institution assembly and September inflation readings ought to go an extended method to firming up bets that Banco de la República turns into the fourth of the area’s massive inflation-targeting central banks to start unwinding report climbing cycles.

Economists surveyed by the central financial institution see a quarter-point minimize to 13% in October and a year-end charge of 12.5%. The early consensus places the September inflation print at simply round 11% from the March cycle excessive of 13.34%.

–With help from Laura Dhillon Kane, Jeremy Diamond, Paul Jackson, Robert Jameson, Piotr Skolimowski, Monique Vanek and Paul Wallace.

(Updates with Peru inflation in Latin America part)

[ad_2]